Finance

May 12 2026

More than half of American consumers are now using credit card debt to pay for essential expenses, not discretionary purchases, according to a 2025 Achieve Center for Consumer Insights study of 2,000 respondents. For retail, this signals a structural contraction in discretionary demand. Brands that fail to pivot toward value-led messaging, flexible payment terms, and cost-per-use positioning risk losing ground

Arthur Zaczkiewicz

More than half of American consumers are now using credit card debt to pay for essential expenses, not discretionary purchases, according to a 2025 Achieve Center for Consumer Insights study of 2,000 respondents. For retail, this signals a structural contraction in discretionary demand. Brands that fail to pivot toward value-led messaging, flexible payment terms, and cost-per-use positioning risk losing ground to private-label and discount alternatives.

A new report released by digital personal finance firm Achieve revealed that more than half of American consumers are currently carrying credit card balances to manage the rising costs of essential living expenses. And it doesn’t bode well for retailers and brands.

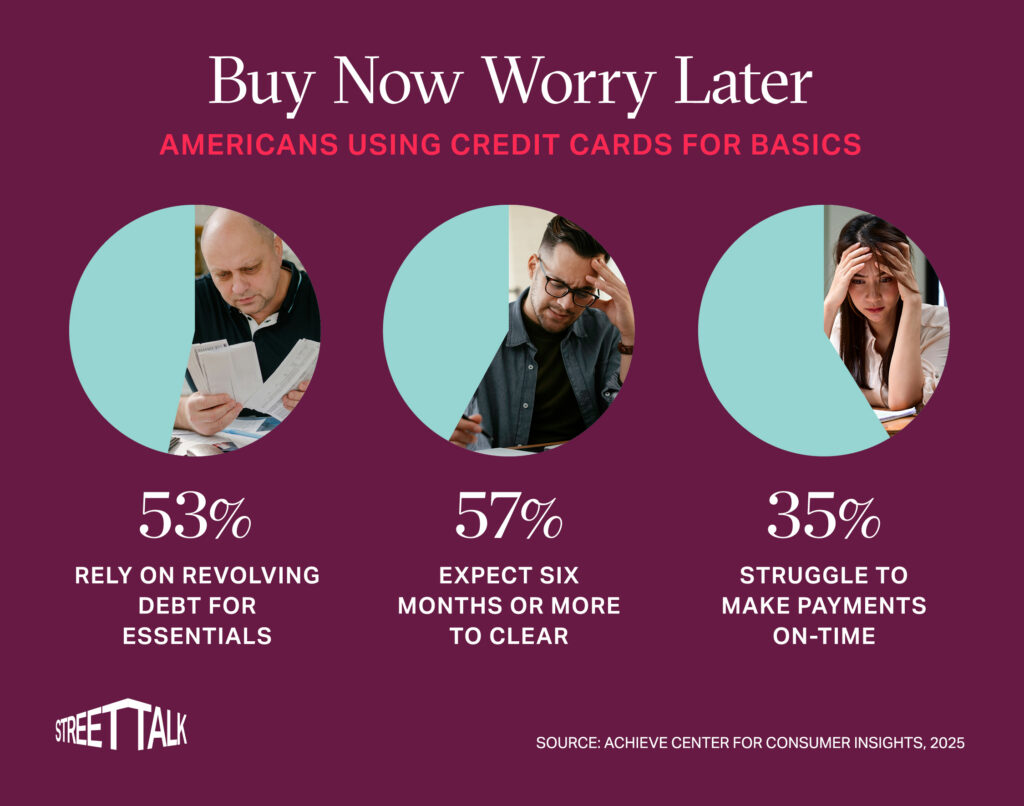

The survey, conducted by the Achieve Center for Consumer Insights, found that 53% of respondents rely on revolving debt not for discretionary splurges, but as a necessary coping mechanism to afford everyday necessities.

What Does the Achieve Consumer Debt Study Actually Show?

The findings spotlight a growing trend of financial strain on households as inflation continues to impact family budgets. According to the study, 25% of those surveyed have been carrying these balances for six months or longer while 57% of consumers estimate it will take them at least half a year to pay off their short-term unsecured debts, which includes credit cards, personal loans and “buy now, pay later” plans.

This represents a slight increase from the first quarter of the year, signaling that debt cycles are becoming harder to break for many households.

Austin Kilgore, an analyst for the Achieve Center for Consumer Insights, said the rising credit card usage in the current climate is often a sign of financial struggle rather than consumer confidence. He explained that many consumers are finding it increasingly difficult to reduce their spending further, as nearly half of the respondents reported that they cannot realistically cut back any more on essential bills and utilities.

How is Debt Stress Changing the Way Consumers Shop?

The survey revealed that 51% of consumers polled said they feel “uncomfortable” or “extremely uncomfortable” using credit cards for essential expenses when they cannot pay the balance in full immediately. Additionally, 35% of respondents described maintaining on-time debt payments as a difficult or very difficult task, reflecting a precarious financial situation for a significant portion of the population.

This qualitative study of 2,000 consumers was designed to complement official data on household debt by providing a deeper look into the motivations behind consumer borrowing. As everyday costs remain high, the report suggests that for many U.S. consumers, the divide between income and essential expenses is being bridged by high-interest debt that may take months or even years to resolve.

What Should Retailers Do When Customers are Borrowing to Buy Essentials?

For retailers and brands, these findings signal a critical shift in consumer behavior that calls for a move away from traditional high-volume growth strategies. As more shoppers bridge the gap between income and necessities with credit, discretionary categories such as apparel, home decor and electronics are likely to see continued softening. Brands can no longer rely on the assumption of “revenge spending” or impulse buys. Instead, they must focus on value-driven messaging and loyalty programs that provide tangible financial relief. Companies that fail to acknowledge the liquidity crunch facing their customers risk losing market share to private-label alternatives and discount competitors as consumers prioritize survival over brand affinity.

Additionally, the increased reliance on buy now, pay later and revolving credit suggests that the point-of-sale experience is becoming as much about financing as it is about the product itself. Retailers may find that offering flexible payment terms is no longer a perk but a requirement for conversion.

However, there is a delicate balance to strike, as over-extending credit to a stressed consumer base could lead to higher return rates or long-term brand erosion if customers begin to associate specific retailers with their mounting debt. In this environment, brands that emphasize durability and “cost-per-use” will likely resonate more effectively than those pushing fast-fashion or short-lived trends.

Related articles: Resilience Amid Rising Costs: Massachusetts Leads U.S. in Consumer Spending

The Street Talk newsletter delivers the sharpest fashion, beauty, and retail analysis every Thursday — straight from Arthur Zaczkiewicz, former Executive Editor at WWD. Subscribe today.